We have started to look at the original Newman Brothers accounting ledgers and have done some preliminary work to analyse the figures.

This isn’t an accounting exercise as such but is to try and find the stories behind the figures, for example:

- How successful was the business in financial terms?

- When did they change from gas engines to electric motors?

- How much did they spend on wages each year?

- How much rent was paid to the Colmore Estate?

- When did they stop sand casting?

Even a brief overview of the accounts has thrown up a number of questions, we will try to address through a series of blogs over the coming months.

NET PROFIT:

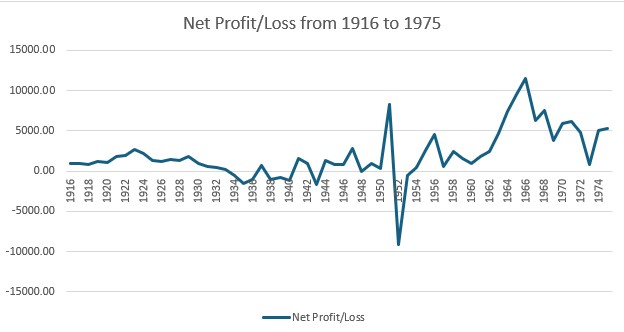

As an introduction the first figure to look at is the Net profit. This is the “bottom line” and is a measure of the financial success of the business. It is the sales figures add any sundry, or miscellaneous income less all production costs and other expenses and is the amount that the owners are able to draw on as drawings or dividends. The Net profit below only goes up to 1975 as that is all the information we have found in the records so far.

The net profit increased from £969 in 1916 to £2682 in 1923 but then fell steadily until 1934 when there were three consecutive years of losses. This coincided with incorporation of the business when it became a limited company in 1933. There followed several years, for the rest of the 1930s and 1940s, of mixed results with profits and losses, all under £3000. This is interesting as the narrative has always been that the 1930s were boom years, but this wasn’t the case according to the accounts.

Then in 1951 there was a huge net profit of £8293 followed by a huge loss of £9112 the next year – this needs investigating. After that, until 1962, there were relatively small profits until, in 1963 they started to climb again reaching a peak of £11,516 in 1966 before gradually falling to £5264 in 1975. However, the sales also went up over this period and net profit broadly followed these movements in sales.

There are many factors affecting the net profit including sales, wages costs, material costs and general expenses as well as the economy, trading conditions etc. This is an ongoing project that we will be undertaking over the next twelve months looking at one area at a time and giving regular updates.

By Lindsay Whitlow, Volunteer